It’s a crisp Friday morning in February 2026. You wake up, brew a pot of coffee using power harvested from your roof, and look out the window at a pristine landscape untouched by power lines or utility poles. There’s a distinct feeling of freedom that comes with knowing you aren’t reliant on the grid, and you certainly aren’t missing those monthly utility bills.

This is the dream of off-grid living, and it is becoming more popular by the day. In fact, recent reports on solar adoption suggest that interest in fully off-grid lifestyles has grown by nearly 20% in 2025 alone. People are tired of rising energy costs and are looking for resilience, self-sufficiency, and a smaller carbon footprint.

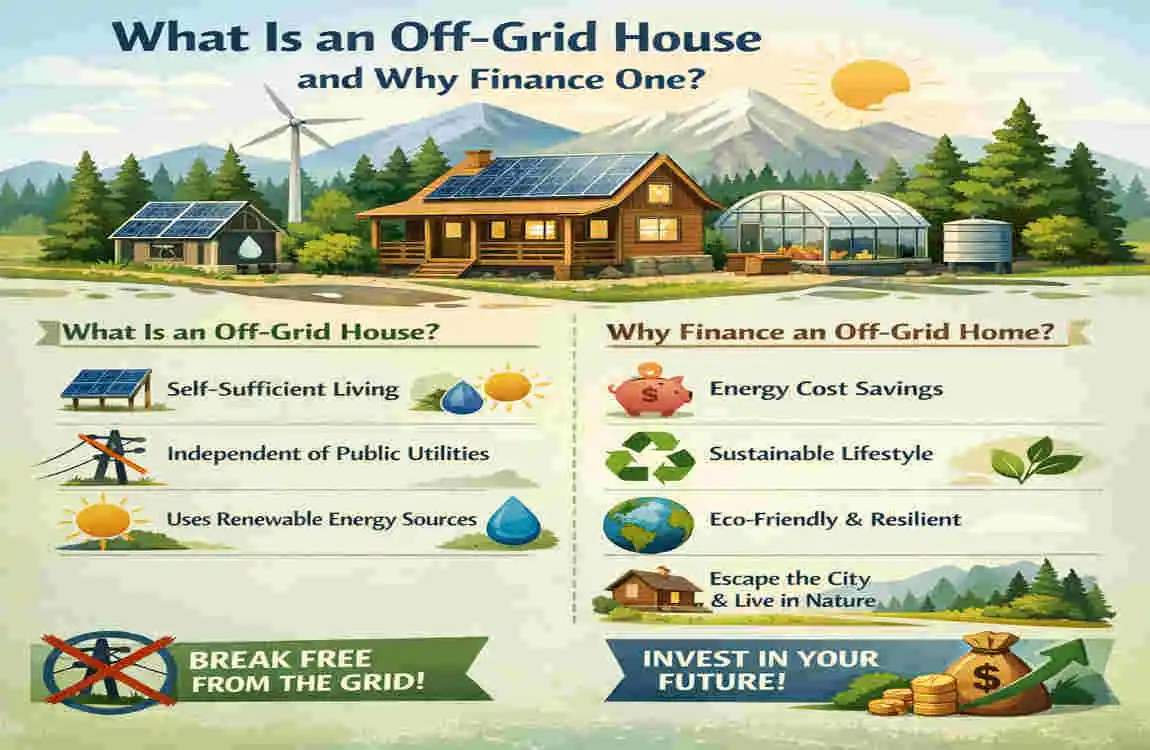

What Is an Off-Grid House and Why Finance One?

Before we dive into the nitty-gritty of paperwork and interest rates, let’s make sure we are on the same page about what an off-grid house actually is.

In the past, “off-grid” might have conjured images of a rustic shack with a wood stove and an outhouse. Today, that definition has evolved. A modern off-grid house is a fully functional home that operates independently of public utilities. It generates its own electricity (usually from solar or wind), sources its own water (from wells or rainwater catchment), and manages its own waste (with septic systems or composting toilets).

Many of these homes are just as comfortable—if not more so—than their grid-tied neighbors. They happen to be self-sufficient.

Why Are People Making the Switch?

The motivation usually comes down to three things: freedom, finances, and the future.

When you cut the cord, you gain energy independence. You are no longer at the mercy of rolling blackouts or storm-induced power failures. Plus, the environmental impact is significantly lower. But for many, the biggest draw is the financial savings. By eliminating monthly electric, water, and gas bills, homeowners can save $2,000 to $3,000 per year on utilities, depending on their location.

However, reaching that level of savings requires a significant initial investment.

The Financial Reality: Pros and Cons

If you are planning to pay cash, you are in the minority. Most people need help covering the upfront costs.

The Pros of Off-Grid Living:

- Zero Utility Bills: Once the system is paid for, your energy is free.

- Resilience: Your lights stay on when the rest of the county goes dark.

- Tax Incentives: Even in 2026, federal and state tax credits for solar and battery storage can offset installation costs.

The Cons (and Why You Need a Loan):

- High Upfront Costs: A robust off-grid power system (panels, inverters, massive battery banks) can easily add $50,000 to $200,000 to the cost of a home build.

- Maintenance: You are your own utility company, meaning repairs are on your dime.

Building a standard home is expensive enough, but when you add the specialized systems required for self-sufficiency, the average off-grid build can cost $300,000 to $500,000. Most of us don’t have that kind of cash sitting under the mattress.

This brings us back to the central problem. You know you want to do it, and you know it makes financial sense in the long run. But can you get a loan for an off-grid house to make it happen right now? Let’s break it down.

Can You Get a Loan for an Off-Grid House? The Short Answer

However, it is not as simple as walking into a big-box bank and signing a standard 30-year fixed mortgage application. While it is possible, you are going to face more hurdles than the average homebuyer.

Lenders are in the business of risk management. When they lend you money, the house acts as collateral. If you stop paying, they take the house and sell it to get their money back. Lenders get nervous about off-grid homes because they worry about marketability. They ask themselves, “If we have to foreclose, will anyone else want to buy a house that runs on batteries and well water?”

Factors Lenders Assess

To get a “yes,” you need to prove that your home is a solid investment. Lenders will look closely at:

- Property Type: Is it a permitted, legal residence, or a temporary structure?

- Energy Independence: Can you prove the system provides reliable power year-round?

- Location: Is it accessible by road, or is it miles deep in the wilderness?

Busting the Major Myth

There is a common misconception that government-backed loans, such as FHA or VA, are strictly off-limits for off-grid homes. This is false.

FHA and VA guidelines do not explicitly ban off-grid properties. However, they do require that the home has a continuous and sufficient supply of potable water and sanitary facilities. For electricity, they often require that the home be “grid-tied capable” or that the off-grid system meet strict local building codes and be accepted by the local market.

If you can demonstrate that off-grid homes are common in your area (using “comps” or comparable sales), your chances of approval skyrocket.

Here are a few quick wins to keep in mind:

- 70% of off-grid loans are approved through construction-to-permanent financing or land loans, rather than traditional mortgages.

- Local credit unions and specialized lenders are much more likely to approve you than national banks.

- Yes, you can get a loan for an off-grid house through niche lenders if you present a professional, well-documented plan.

Main Financing Options for Off-Grid Homes

Since a standard mortgage might not fit, you should consider loan products designed for non-traditional homes. Let’s dive deep into the best options available in the 2026 market.

Construction-to-Permanent Loans

If you are building your off-grid sanctuary from scratch, this is often the gold standard. A Construction-to-Permanent loan (often called a “single-close” loan) combines financing for the purchase of the land and the construction of the home into one single loan.

Once the building is finished, the loan automatically converts into a standard mortgage.

- Why it works: It covers the high upfront costs of your solar panels, septic system, and well drilling as part of the total build cost.

- The Catch: You will need a large down payment (often 20%) and detailed plans from a licensed builder.

USDA Rural Development Loans

For many off-grid enthusiasts, the USDA loan is the holy grail. These loans are designed specifically to encourage development in rural areas—exactly where you are likely to build an off-grid home.

- The Benefit: They offer 0% down payment options.

- The Requirement: The property must be in a designated “rural” area, and the home must meet strict safety standards. You will have to prove that your off-grid systems (water and power) are functionally equivalent to public utilities.

FHA 203(k) Loans

If you are buying an older cabin and want to renovate it into a modern off-grid home, the FHA 203(k) loan is a fantastic tool. It allows you to wrap the purchase price and renovation costs into a single mortgage.

- Flexibility: You can use the renovation funds to upgrade insulation, install solar panels, or drill a new well.

- Credit Friendly: FHA loans generally allow lower credit scores than conventional loans.

Owner-Builder Loans

Are you planning to swing the hammer yourself? Most banks hate this because they trust licensed contractors more than DIYers. However, Owner-Builder loans do exist.

- How it works: You act as your own general contractor.

- Difficulty: These are very hard to find and often require a background in construction. The interest rates are typically higher to offset the risk that you might not finish the house.

Personal Loans and Home Equity

Sometimes, you might get a mortgage for the “shell” of the house, but the bank won’t cover the solar system. In this case, you can use personal loans or HELOCs (if you have another property) to bridge the gap.

Comparison of Off-Grid Financing Options (2026 Estimates)

Here is a comparison of how these loans stack up in the current market.

Loan Type Best For Pros Cons Typical Rates (2026)

Construction-to-Permanent New custom builds One-time closing costs; covers full solar install Strict inspections & higher down payment 6.5% – 7.5%

USDA Rural Loans Remote/Rural properties 0% Down Payment; low mortgage insurance Income limits & strict location rules 6.0% – 7.0%

FHA 203(k) Renovating existing homes , Flexible funds for off-grid upgrades , Higher fees (MIP); strict appraisal 6.25% – 7.25%

Owner-Builder Loans DIY enthusiasts You control the build; custom terms Hard to qualify; higher interest rates 7.0% – 9.0%

Personal / Home Equity Filling funding gaps Fast funding; no property appraisal needed Shorter repayment terms; higher rates 8.0% – 12.0%

Top Lenders and Programs for Off-Grid House Loans

Knowing the loan type is half the battle; finding a lender who won’t hang up on you is the other half. You need to target institutions that understand energy efficiency and rural living. Here are the top categories of lenders to approach.

Government-Backed Options

You should always start here because the terms are usually the best.

- Fannie Mae / Freddie Mac: Believe it or not, both of these giants have “Green” initiatives. Their “HomeStyle Energy” mortgage can help you finance energy upgrades. As long as your off-grid home is comparable to other homes in the area, they can purchase the mortgage.

- VA (Veterans Affairs): If you are a veteran, the VA loan is unbeatable. While they have strict “property requirements,” many veterans have successfully used VA loans for off-grid homes by ensuring the water and sewage systems meet local health authority standards.

Credit Unions and Local Banks

This is your secret weapon. Small, local banks in rural areas know the local market.

- Alliant Credit Union: Known for being very friendly toward tiny homes and alternative living structures. They often have portfolio loans (loans they keep on their own books rather than sell to Wall Street), which give them greater flexibility.

- Navy Federal Credit Union: Another excellent option for military families with flexible lending criteria.

- Local Rural Banks: If you are building in a specific county, visit the community bank in the county seat. They likely have financed other off-grid properties nearby and won’t be scared by your proposal.

Specialty Green Lenders

In 2026, several lenders specialize strictly in green energy financing. While they might not finance the whole house, they can finance the expensive systems (solar, wind, batteries).

- LightStream: They offer unsecured loans up to $100,000 for “green” projects. This is great for buying your power system if your mortgage doesn’t cover it.

- GoKapital: A lender that offers various business and hard money loans, often used by real estate investors for non-traditional properties.

Renewable Energy Financiers

Companies like Mosaic and Dividend Finance focus specifically on solar loans. They offer terms ranging from 10 to 20 years. If you can get a mortgage for the structure but not the solar, these guys can fill the gap.

Real Case Example: Consider “John,” a resident of rural Colorado. He found a beautiful plot of land, but the big banks rejected his application because the nearest power pole was three miles away. He approached Alliant Credit Union. Because he had a solid credit score and a detailed plan from a certified solar installer, Alliant approved a $350,000 loan. He also utilized the 30% Federal Solar Tax Credit to recoup some of the costs the following year.

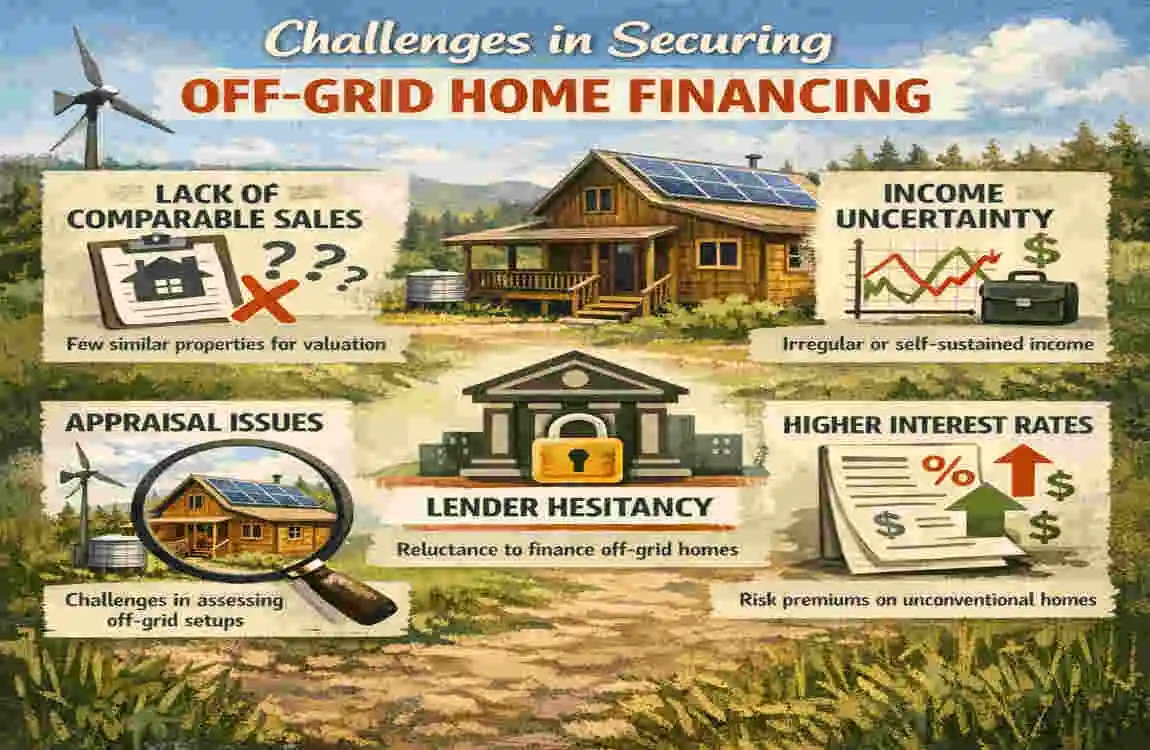

Challenges in Securing Off-Grid Home Financing

I want to be honest with you—it’s not going to be a walk in the park. You will face rejection, and you need to be prepared to answer tough questions. Here are the main pain points you will encounter.

The Appraisal Nightmare

This is the number one reason off-grid loans are denied. Appraisers determine a home’s value by comparing it to recently sold homes nearby (Comps).

- The Problem: If you build a unique off-grid dome home in an area where everyone else lives in standard grid-tied ranch houses, the appraiser has nothing to compare it to. They might value your $50,000 solar system at $0 because they don’t understand it.

- The Fix: You must hire an appraiser with a specific green building certification. You may have to pay extra for this, but it is essential.

Insurance Issues

You cannot get a mortgage without homeowner’s insurance. However, many insurers are wary of off-grid homes due to fire risks (especially in remote wooded areas) and the lack of a nearby fire hydrant.

- The Fix: Look for “FAIR” plans (state-mandated insurance for high-risk areas) or bundle your insurance with a company that specializes in rural properties.

Zoning and Title Issues

Before you apply for a loan, you must ensure it is legally possible to live off-grid on your land. Some municipalities require a connection to the grid for a certificate of occupancy.

- The Fix: Visit your county zoning office first. Get a letter stating that off-grid living is permitted.

Utilities Availability

Lenders want to know what happens if your solar panels break.

- The Fix: Redundancy. Show them you have a backup generator and a wood stove. Prove that the house is habitable even if the sun doesn’t shine for a week.

10 Expert Tips to Get Approved for Your Off-Grid Loan

If you want to increase your odds from “maybe” to “approved,” follow this checklist. These are tips gathered from industry experts and successful off-grid homeowners.

- Document Your Systems: Don’t just say “solar power.” Provide spec sheets, invoices, and warranty information for every battery and panel. Show the lender that this is professional-grade gear, not a science fair project.

- Get Pre-Approved by 3 Lenders: Do not put all your eggs in one basket. Apply to a credit union, a government-backed lender, and a local bank simultaneously.

- Boost Your Credit Score: Because the property is “risky,” you need to be “safe.” Aim for a credit score of 680 or higher to give the lender confidence.

- Add a “Grid-Tie” Option: Even if you never plan to use it, having the infrastructure to connect to the grid (if it’s nearby) can ease a nervous lender’s mind.

- Use Energy Modeling Software: Provide a report showing exactly how much power your system will generate versus how much the house needs. Numbers build trust.

- Partner with Certified Builders: If you are building, use a contractor with a track record of green builds. Lenders trust established businesses more than owner-builders.

- Apply for Grants: Look into programs like the USDA REAP (Rural Energy for America Program). While primarily for businesses, there are residential off-grid grants and rebates available that can lower your loan amount.

- Shop During Off-Peak Seasons: Construction loans are often processed more quickly in the winter, when builders are less busy.

- Prove Resale Value: Find examples of recently sold off-grid homes in the region. If you can do the appraiser’s homework for them, you win.

- Consult an Off-Grid Loan Broker: There are mortgage brokers who specialize in “non-conforming” properties. They know exactly which lenders are hungry for this type of business.

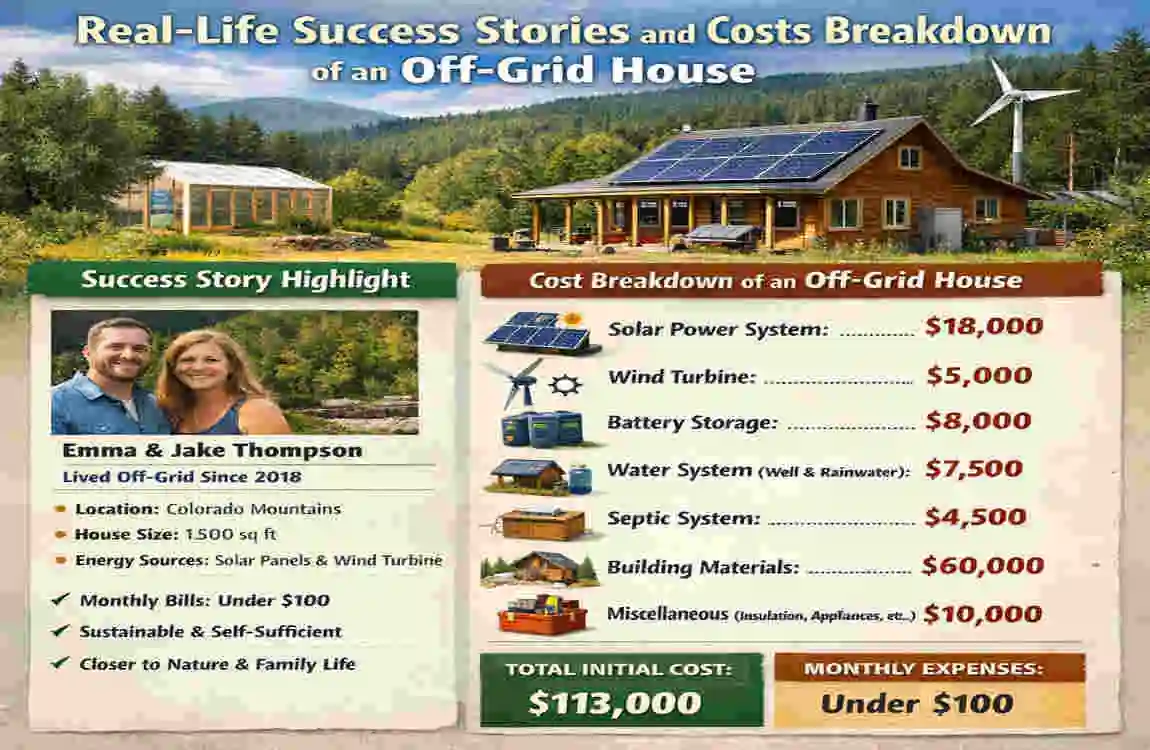

Real-Life Success Stories and Costs Breakdown

Muhammad in Lahore: Muhammad wanted to build an eco-friendly home outside of Lahore to escape the city’s smog and unreliable grid. Traditional banks were skeptical of his “hybrid” mud-brick and solar design. He turned to a specific green financing initiative offered by a local bank that supports renewable energy infrastructure. By proving his solar setup would save him 40% on energy costs compared to a city apartment, he secured financing. His home is now a model for sustainable living in the region.

Sarah in Oregon: Sarah used a USDA Direct Loan to buy a remote cabin. The cabin had no power lines. She used the loan to purchase the property and a separate personal loan from Light Stream to install a $40,000 solar array. Today, her total monthly loan payment is lower than the rent she used to pay in Portland.

Cost Scenario: The Break-Even

Here is a quick look at why the loan is worth it.

ItemStandard Home CostOff-Grid Home Cost

Grid Connection $5,000 – $15,000 $0

Monthly Electric $150 – $250 $0

Monthly Water $50 – $100 $0

Solar/Well Install $0 $45,000 (Financed)

10-Year Savings -$30,000 (Paid to Utility) +$30,000 (Asset Value)

While the off-grid home costs more upfront, the money you would have paid to the utility company goes toward paying off your own asset instead.

FAQ: Can You Get a Loan for an Off-Grid House?

Q: Can you get a conventional mortgage for an off-grid house? A: Generally, no. Big national banks usually require homes to be connected to public utilities. However, you can get financing through USDA rural loans, construction-to-permanent loans, or local credit unions that understand the local market.

Q: Do FHA or VA loans allow off-grid living? A: Yes, but there is a catch. The home must meet strict safety and health standards. You must prove you have a continuous supply of potable water (tested well water) and a sanitary sewage system. For VA loans, the property must also be accessible by an all-weather road.

Q: Why do lenders deny off-grid loans? A: The main reason is comparable sales (comps). To approve a loan, an appraiser needs to see that other similar off-grid homes in the area have sold recently. If you are the only off-grid house for 20 miles, the lender views it as a “risky” investment because they aren’t sure of its resale value.

Q: Can I get a loan just for the solar panels and batteries? A: Yes. If you can’t bundle the energy system into your main mortgage, you can use specialized green lenders (like LightStream or Mosaic) or a personal loan to finance the equipment separately.

Q: Is it harder to get insurance for an off-grid home? A: It can be. Many major insurers hesitate if the home is far from a fire hydrant or fire station. You may need to look for “FAIR” plans (state-run insurance for high-risk areas) or specialty insurers who cover rural properties.

Q: How much down payment do I need? A: It depends on the loan.

- USDA Loans: 0% down.

- FHA Loans: 3.5% down.

- Construction/Land Loans: Typically 20% to 30% down because they are considered higher risk.