The home-selling process can be both exciting and nerve-wracking. You’ve invested time, effort, and money into preparing your property, and when the offers start coming in, it’s a moment of relief. However, accepting an offer is just one step in a complex journey, and it comes with its own set of risks and considerations.

Selling a home is often one of the most significant financial transactions in a person’s life. While finding a buyer and accepting an offer may feel like the finish line, it’s just the beginning of a new phase. Many sellers are unaware of the potential risks and complications arising after accepting an offer.

The Home Selling Process: From Listing to Offer Acceptance

Selling a home involves multiple steps, each critical in securing a successful sale. Here’s an overview of the process leading up to accepting an offer:

Listing the Property

The journey begins with listing your property. This step involves setting a competitive asking price, preparing your home for showings, and marketing it effectively. A well-staged and strategically priced home attracts more buyers, increasing your chances of receiving strong offers.

Marketing and Showings

Once your home is listed, real estate agents use marketing strategies to showcase the property. This includes online listings, open houses, and private showings. These efforts aim to generate interest and encourage potential buyers to submit offers.

Receiving Offers

When buyers are interested, they submit offers that include their proposed purchase price, contingencies, and timelines. As a seller, you’ll review these offers and choose the one that best suits your needs. This is where the concept of “accepting an offer” comes into play.

What Does It Mean to “Accept” an Offer?

Accepting an offer typically means that you, as the seller, have agreed to the terms proposed by the buyer. However, it’s important to distinguish between verbal acceptance and written acceptance:

- Verbal Acceptance: Informal and not legally binding in most cases.

- Written Acceptance: A signed agreement that solidifies the terms and begins the formal transaction process.

Additionally, offers can be conditional (subject to contingencies like inspections or financing) or unconditional (no contingencies, often seen in competitive markets).

Real estate agents and lawyers are crucial in guiding you through this stage, ensuring you understand the implications of accepting an offer.

What Happens Once an Offer Is Accepted?

After you’ve accepted an offer, the home sale process moves into its next phase. This involves several key steps, each of which can carry risks if not handled carefully.

Timeline of Events After Offer Acceptance

Here’s what typically happens once you’ve accepted an offer:

- Deposit Transfer: The buyer provides an earnest deposit to demonstrate their commitment to the purchase.

- Mortgage Approval: The buyer works with their lender to secure financing.

- Home Inspection and Appraisal: The buyer may arrange a home inspection and appraisal to ensure the property meets their expectations and the lender’s requirements.

- Removal of Contingencies: If the offer is conditional, the buyer must meet the outlined contingencies within the agreed timeframe.

- Final Paperwork and Closing: Once all conditions are met, the transaction moves toward closing, where the property officially changes hands.

Legal Status of the Transaction

The transaction is not set in stone until the sale is legally finalized (usually at closing). This means there’s potential for complications or even the deal falling apart.

Buyer and Seller Obligations

Both parties have responsibilities during this stage:

- The buyer must fulfill their contingencies and secure financing.

- The seller must ensure the property is in the agreed condition and cooperate with inspections or appraisals.

Can Someone Else Make an Offer After Acceptance?

This is a critical question for many sellers: once a house is accepted, can someone else make an offer?

The Legal and Practical Realities

The short answer is yes; someone else can make an offer even after you’ve accepted one. However, whether you, as the seller, can legally consider or accept this new offer depends on the terms of the initial agreement and local laws.

In most cases:

- If you’ve signed a binding contract, you are legally obligated to honor it. Walking away to accept a better offer could result in legal consequences.

- In some regions, such as Scotland, once an offer is accepted, the property is considered legally off the market, and accepting another offer is not permitted.

Backup Offers

While you can’t arbitrarily walk away from a signed agreement, backup offers can play a role. These offers are made by other interested buyers who agree to step in if the original deal falls through. Backup offers provide a safety net for sellers without breaching contractual obligations.

When Another Offer Can Be Considered

In rare cases, if the original buyer fails to meet their obligations (e.g., by not securing financing), the seller may have the opportunity to consider new offers.

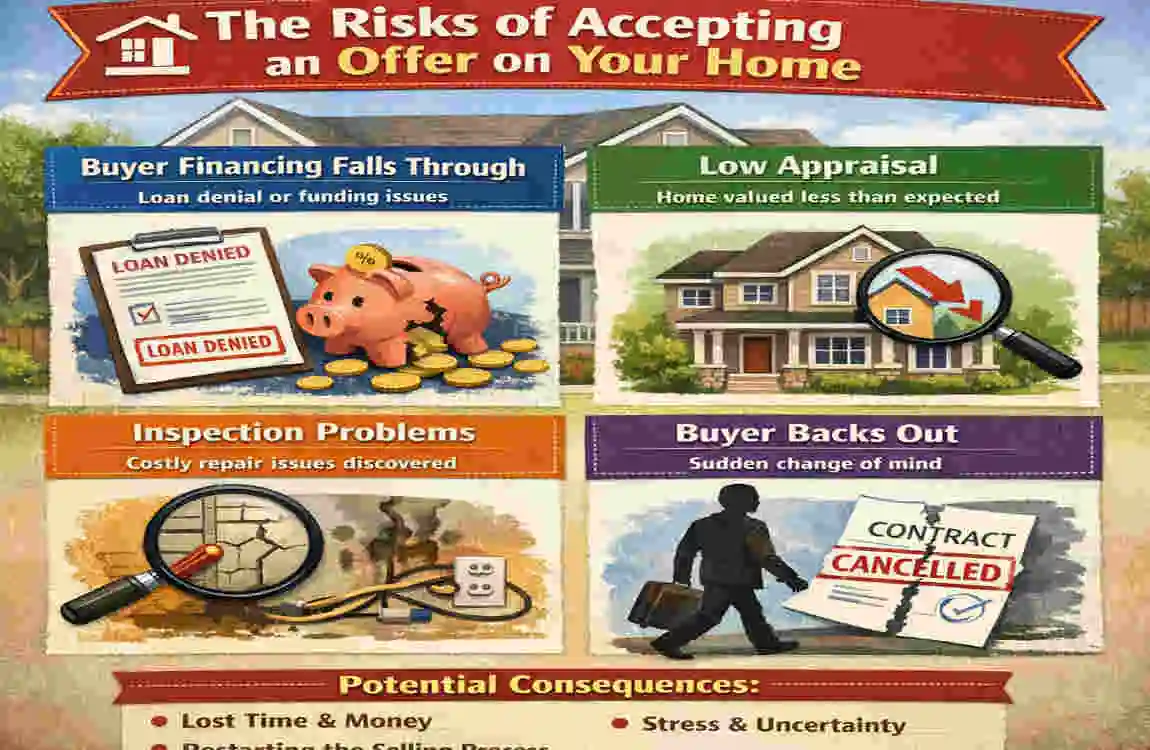

The Risks of Accepting an Offer on Your Home

While accepting an offer can feel like a significant milestone, it comes with potential risks. Here’s what you need to know:

Risk of Higher Offers After Acceptance

One of the most common concerns is seller’s remorse, which occurs when a better offer comes in after you’ve already accepted one. Reneging on an accepted offer can have serious legal and ethical implications.

Risks Related to Buyer Financing and Contingencies

- Buyers might fail to secure their mortgage, jeopardizing the sale.

- Contingencies, such as inspection results or the buyer’s need to sell their current home, can lead to delays or renegotiations.

Risk of Transaction Falling Apart

If the buyer backs out, the seller may face challenges, such as:

- Losing time on the market.

- Re-listing the property can create a stigma.

Legal Risks

Failing to honor a legally binding agreement could lead to lawsuits. Sellers should work with an attorney to avoid breaches of contract.

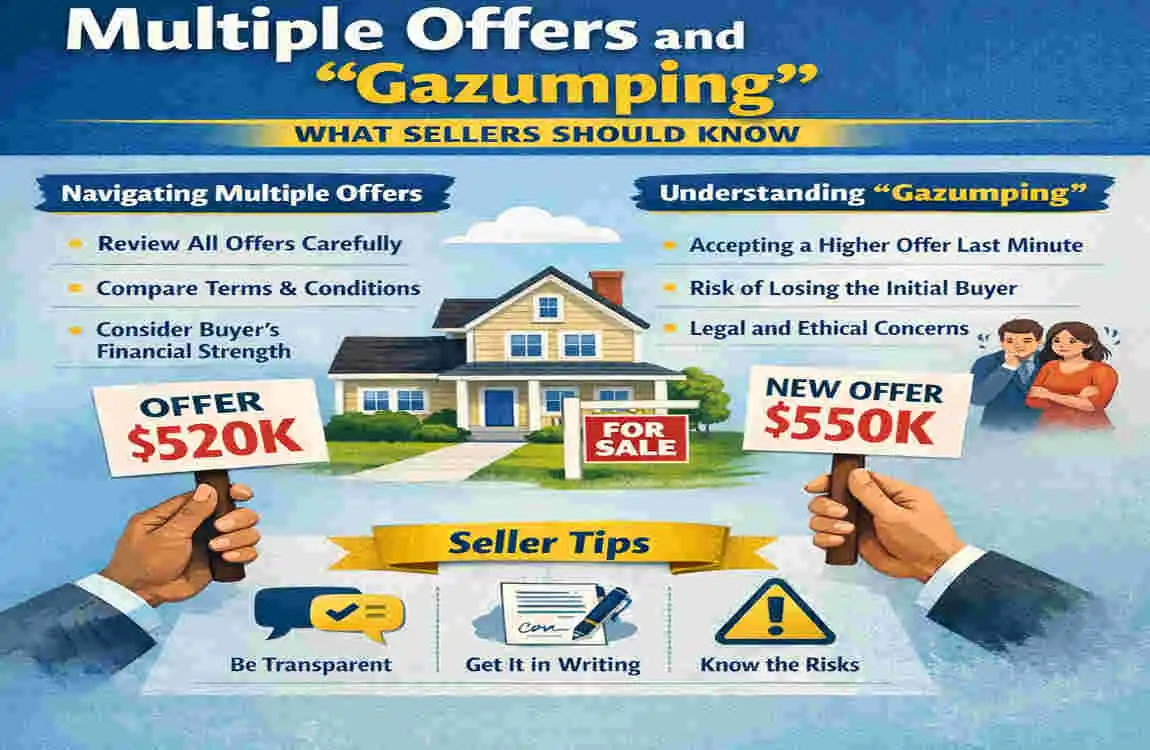

Multiple Offers and “Gazumping”: What Sellers Should Know

What Is Gazumping?

Gazumping occurs when a seller accepts a higher offer after agreeing to one. While legal in some areas, it’s widely considered unethical.

Handling Multiple Offers

Real estate agents often recommend setting clear deadlines for offers and consulting with professionals to navigate multiple offers ethically.

Scenario Action

A higher offer comes in Consult your agent and understand the legal implications of reneging.

Backup offer is present Use it as a safety net without breaching your current agreement.

Market conditions change Reassess your options with your agent but honor existing commitments.

Protecting Yourself as a Seller

To minimize risks, consider these steps:

- Evaluate Offers Carefully: Assess contingencies and buyer reliability beyond the price.

- Set Clear Contract Terms: Ensure deadlines and conditions are clearly outlined.

- Work With Professionals: Real estate agents and lawyers can guide you through legal and ethical dilemmas.

Protecting Yourself as a Buyer

Buyers also face risks. To protect yourself:

- Strengthen Your Offer: Include a substantial earnest deposit and limit contingencies.

- Understand Backup Offer Dynamics: Know your rights if another offer is accepted.

- Secure Timely Financing: Avoid delays that could jeopardize your agreement.

Frequently Asked Questions

Can a seller legally accept another offer after accepting one?

Only under specific conditions or if the original buyer fails to fulfill obligations.

What happens if a better offer comes in?

Sellers must honor existing agreements unless contingencies aren’t met.

What is a backup offer?

A secondary offer that becomes active if the primary deal falls through.

Conclusion

Accepting an offer on your home is a significant step, but proceeding with caution is essential. Understanding the risks, legal obligations, and options available can help you navigate this stage successfully. Always consult professionals to ensure you’re making informed decisions.

By carefully evaluating offers, setting clear terms, and working closely with your agent and lawyer, you can protect yourself from common pitfalls and achieve a smooth transaction.