The debate over whether it is more affordable to buy a house or to rent has intensified in recent years, especially as housing markets continue to evolve and financial pressures reshape household budgets. In 2025, new data reveals that despite rising home prices and higher interest rates, owning a home may still be more affordable than renting in many U.S. markets—particularly for those seeking three-bedroom properties. However, this affordability varies by region and depends on individual financial circumstances. This discussion explores the latest trends, weighs the costs and benefits of each option, and helps clarify when buying a house truly offers an economic advantage over renting.

Pros and cons of buying a house

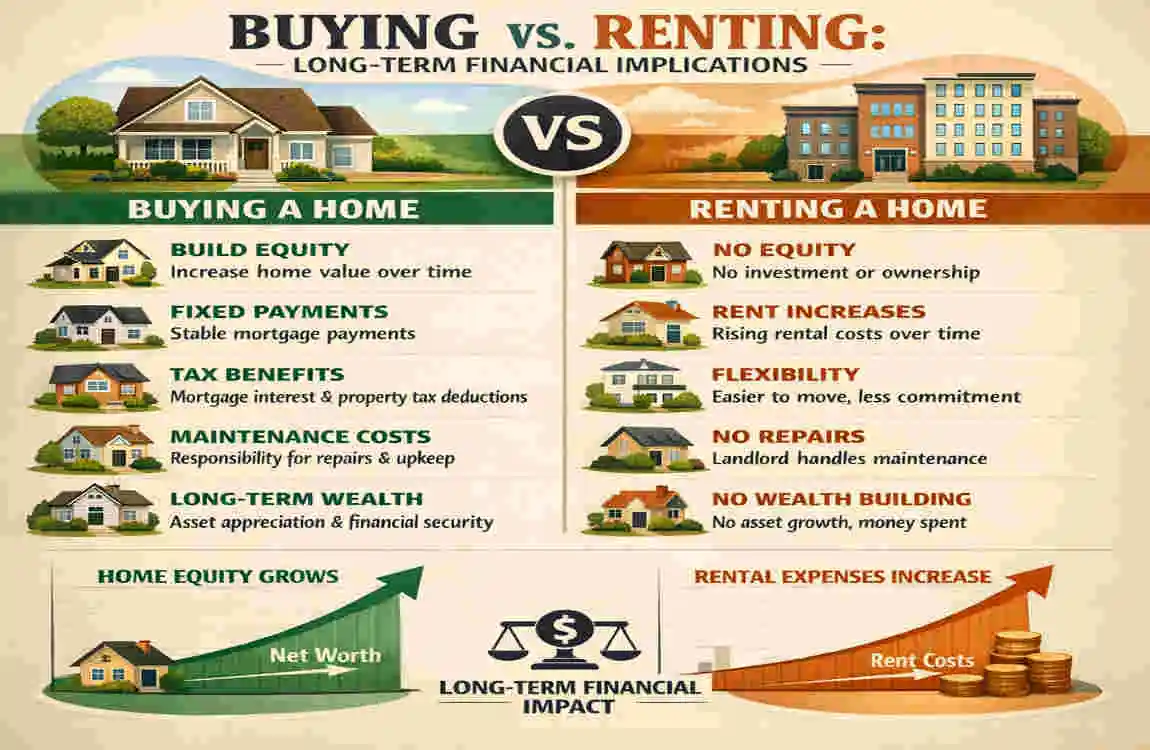

Buying a house can be a rewarding experience. It often means stability and the chance to build equity over time. Homeownership allows for customization, letting you make the space truly your own.

However, there are significant drawbacks to consider. The initial costs—like down payments and closing fees—can be substantial. Ongoing expenses like property taxes, maintenance, and repairs can add up quickly.

Market fluctuations may affect your investment value.

Owning a home ties you more closely to one location. If job opportunities arise elsewhere or personal circumstances change, flexibility becomes limited when mortgage commitments tie you down.

Pros and cons of renting a house

Renting a house offers flexibility. You can relocate easily when your lease ends, which is ideal for those who move frequently for work or personal reasons.

There are also lower upfront costs. Typically, you’ll only need the first and last month’s rent plus a security deposit. This makes renting accessible to many people without hefty savings.

However, renting comes with limitations. You often can’t make significant changes to the property, such as painting walls or renovating spaces.

While living in someone else’s investment, you’re not investing in an asset that could be appreciated over time.

Maintenance responsibilities often fall on landlords. This means fewer worries about repairs and less control over how quickly issues are addressed.

Rental prices can increase at renewal time, impacting long-term budgeting and financial stability for renters relying on fixed incomes.

Factors to consider when deciding between buying or renting

Personal circumstances play a vital role when deciding between buying or renting a house. Assess your financial stability first. A stable income can make mortgage payments manageable.

Consider your lifestyle needs. If you value flexibility and travel often, renting might suit you best. Homeownership ties you down to one location.

Evaluate the real estate market in your area as well. Prices fluctuate based on demand and location, which can influence whether buying or renting a house is cheaper.

Don’t overlook plans, either. Investing in property may be worthwhile if you plan to settle down for several years. On the flip side, leasing could save hassle and costs if change is likely on the horizon.

Think about the maintenance responsibilities of owning a home versus those typically handled by landlords when renting. Each choice carries its own set of commitments and benefits tailored to different lifestyles.

Long-term financial implications of buying vs. renting

Buying a house and renting come with distinct consequences when evaluating long-term financial implications.

Homeownership often builds equity over time. As you pay down your mortgage, the value of your property may appreciate, creating wealth that can benefit you in the future. This growth potential is a significant draw for buyers.

On the other hand, renting offers flexibility without the burden of maintenance costs or property taxes. Your monthly payments typically cover only rent and utilities. However, those payments contribute nothing to ownership or investment.

Consider unexpected expenses as well; homeowners face repairs and renovations while renters rely on landlords for upkeep. These unforeseen costs can impact overall savings significantly.

Consider lifestyle changes—relocations or job opportunities may be easier when a mortgage commitment does not tie you down. Each choice has its merits depending on personal circumstances and future goals.

Case studies: examples of individuals who have chosen to buy or rent

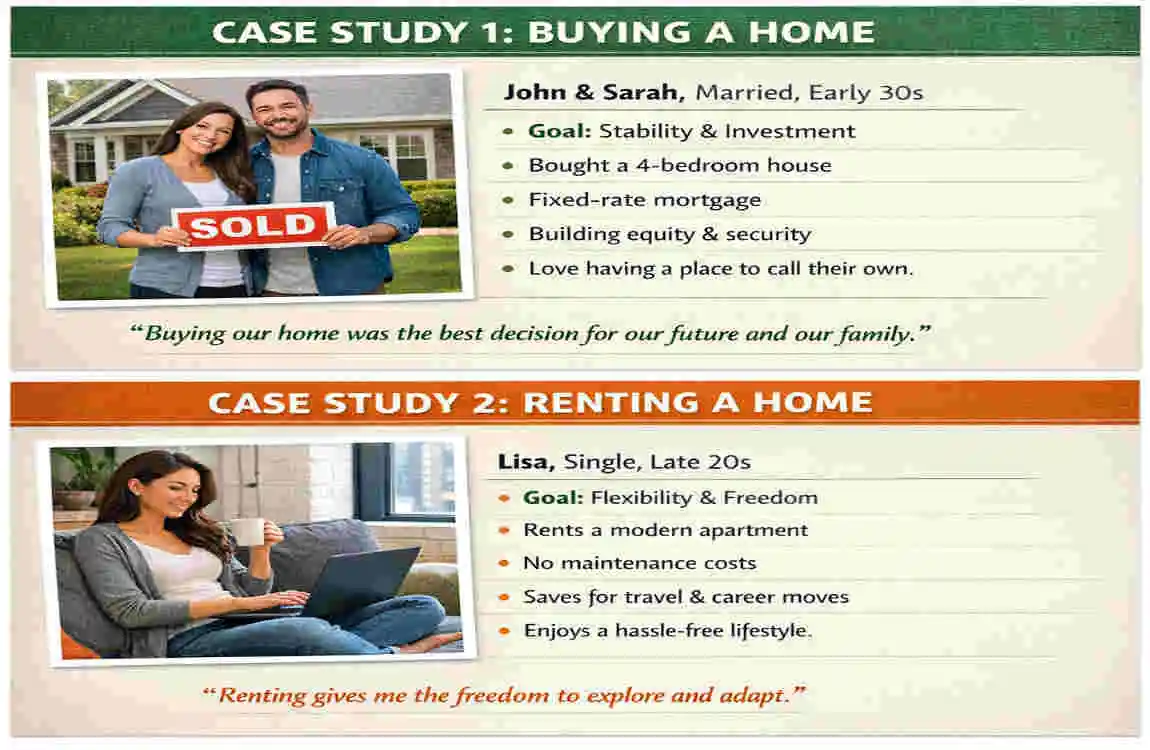

To shed light on the real-world implications of choosing to buy or rent, let’s look at a few case studies that illustrate both paths.

Sarah and Tom are a young couple living in Denver. With stable jobs and a growing family, they purchased their first home after renting for five years. Their monthly mortgage payment is slightly lower than their previous rent, allowing them to invest in renovations that have increased their property value. They appreciate ownership’s stability while enjoying potential tax benefits associated with mortgage interest deductions.

On the other hand, Jason has spent most of his adult life renting apartments in New York City. He enjoys flexibility; he can move easily when job opportunities arise without worrying about selling a house. While his monthly rental payments are higher than some would pay for a mortgage in another city, he appreciates having fewer maintenance responsibilities and no property taxes weighing him down.

Then there’s Linda, who bought a house near her workplace but later realized she wanted more freedom to travel and explore different cities. After just three years as a homeowner, she opted to sell her property at an appropriate time within the market cycle despite facing closing costs and market fluctuations—an experience that taught her valuable lessons about timing in real estate investments.

Each of these individuals made choices based on their lifestyles and financial situations at specific points in time. Buying versus renting houses isn’t purely about numbers; it involves personal circumstances like career goals, family dynamics, community ties, and even emotional well-being regarding homeownership’s long-term commitment.

When considering whether it’s cheaper to buy or rent a house for your situation, take note of Sarah & Tom’s decision toward stability through ownership—and compare this against Jason’s desire for fluidity, which favors renting instead—all leading back to your unique needs today may help steer you toward making an informed choice tailored just right for you!

Is It Cheaper to Buy or Rent a House? FAQ

Q: Is it generally cheaper to rent or buy?

In many places today, renting is cheaper than buying, with studies showing renting is more affordable in nearly all major metros and even cheaper in all 50 states according to recent surveys . Large metros often see rents lower than mortgage payments .

Q: Are there places where buying is cheaper?

Yes. Some markets still show buying can be more cost‑effective long‑term, especially where housing prices are lower and rents are rising .

Q: Does buying become cheaper over time?

It can. With a fixed‑rate mortgage, your monthly payment stays predictable, unlike rent which can rise yearly . You also build equity, which can increase your overall wealth .

Q: What makes renting cheaper upfront?

Renters avoid the big costs of deposits, legal fees, maintenance, and repairs—expenses homeowners must budget for .

Q: What are the financial drawbacks of renting?

Renters don’t build equity, rents may increase, and they have less control over their living space .

Q: What makes buying more expensive right now?

High mortgage rates and rising home prices mean owning is currently more expensive than renting in many major cities .

Q: Which is better in the long run?

Many financial sources say buying is usually better long‑term when you plan to stay put, because the upfront costs balance out over decades and equity grows . But short‑term, renting may be cheaper.