Picture this: You are sitting in a bustling café, sipping a warm cup of chai, and discussing the future with your family. For years, you have been diligently saving up, dreaming of the day you can finally unlock the front door of your very own 5-marla home. But as you look at the real estate trends for 2026, a wave of confusion washes over you. The housing market is moving fast. With property prices experiencing a staggering 20% to 30% annual growth, jumping into the market feels more intimidating than ever.

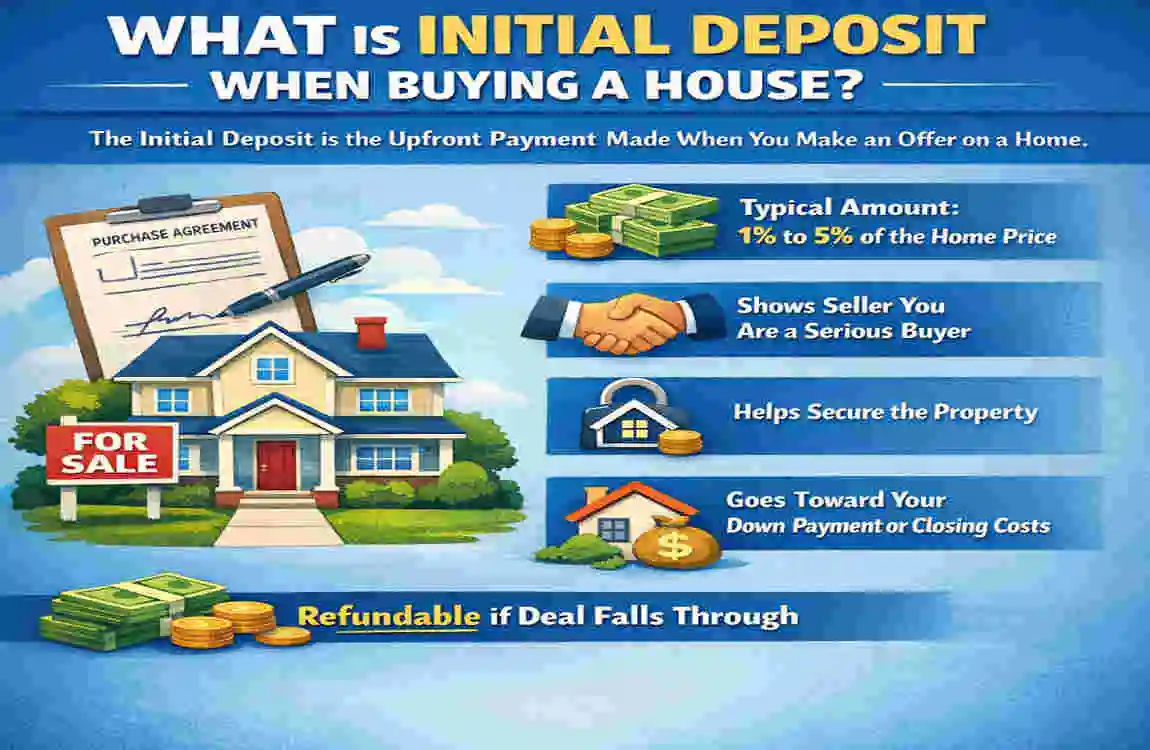

As you start talking to real estate agents and browsing property listings, you are immediately hit with a barrage of financial jargon. The most common phrase you will hear—and likely the most confusing—revolves around upfront costs. You might find yourself frantically searching online, asking, “What is the initial deposit when buying a house?”

To put it simply, your initial deposit consists of two distinct parts: the earnest money you pay to secure the deal, and the larger down payment required by your bank or the seller. Understanding this simple distinction is the master key to unlocking your dream home.

What Is an Initial Deposit When Buying a House?

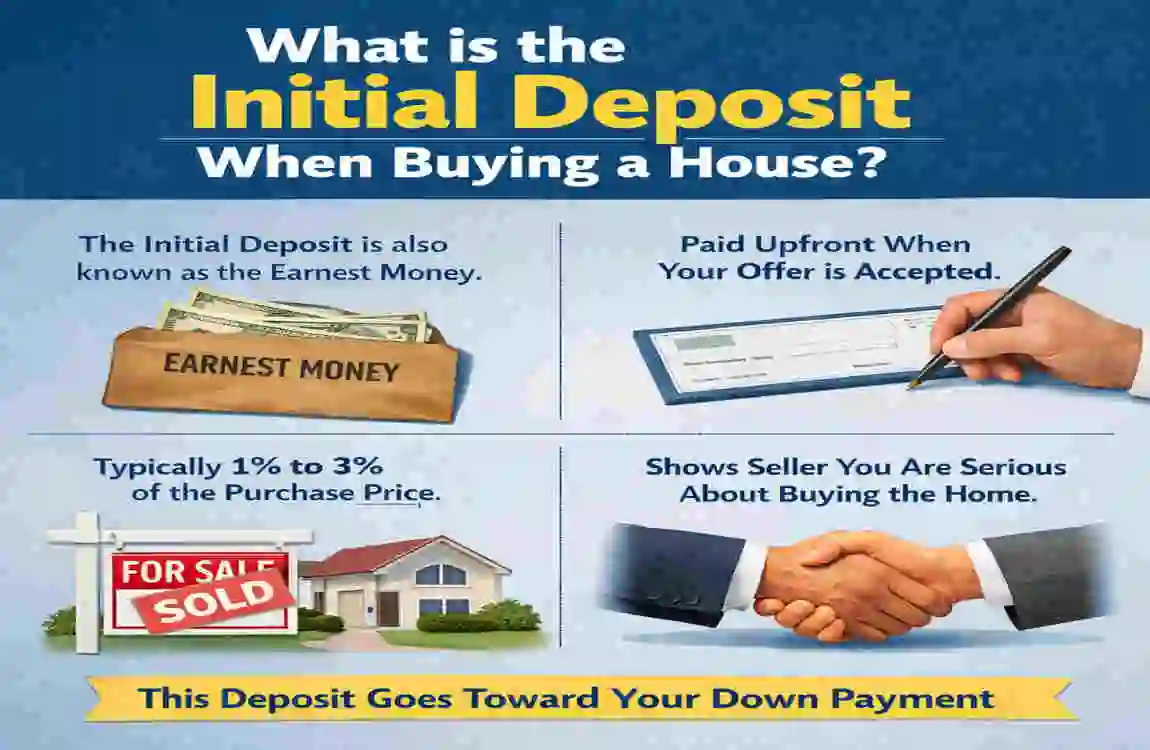

When you finally find that perfect house with the beautiful kitchen and the spacious rooftop, you cannot just shake hands with the seller and move in. You need to put some money on the line to prove that you are a serious buyer. This upfront cash is the initial deposit.

For beginners navigating the real estate market, it is crucial to divide this concept into two distinct categories. Let’s break down the core differences so you can navigate your property meetings with absolute confidence.

Earnest Money vs. Down Payment Explained

Earnest money (often referred to locally as Bayana) is the very first chunk of money you hand over. Think of it as a security deposit that shows your commitment. When you make an offer on a house, and the seller accepts it, you pay this amount to take the property off the market. Usually, earnest money is 1% to 2% of the property’s total value. If the deal falls through because of a valid reason outlined in your contract—like a failed home inspection—this money is typically refundable.

On the other hand, the down payment is the heavy lifter. This is the much larger portion of the home’s purchase price you pay upfront, usually right before or at closing. If you are getting a mortgage, the down payment represents the cash you are contributing, while the bank finances the rest. A standard house down payment ranges from 10% to 30% of the total property value. You finance this through your personal savings, pooling family resources, or utilizing specialized loan programs.

To make things incredibly clear, take a look at this side-by-side comparison:

AspectEarnest Money (Bayana)Down Payment

Amount 1% to 2% (e.g., PKR 200K to 500K) 10% to 30% (e.g., PKR 2M to 10M)

Purpose: To secure the offer and show good faith. To build immediate equity in your new home

Timing: Paid at the initial contract signing stage, paid right before closing or possession

Refundable? Often yes (with contract contingencies). No, it goes directly toward your home equity.

Legal Definition

Under these frameworks, your initial deposit legally locks the property. Once the earnest money is paid and the initial agreement is stamped on legal paper, the seller cannot legally accept offers from other buyers.

Recently, searches for “what is the initial deposit when buying a house” have skyrocketed nationwide. This spike in curiosity is closely tied to the introduction of the Mera Ghar Scheme, which has changed the legal and financial requirements for the deposit a first-time home buyer actually needs. Understanding these local legalities ensures your money is always protected under the law.

How Much Initial Deposit Do You Need?

Now that we know the definitions, let’s talk about real numbers. Exactly how much cash do you need sitting in your bank account before you start house hunting? Let’s look at some realistic breakdowns tailored for the 2026 real estate market.

Average Amounts by Property Size

The amount you need heavily depends on the size of the house you want to buy. In major cities, houses are typically measured in marlas.

If you are looking at a standard 5 Marla house in a decent neighborhood, you can expect to need a total initial deposit (earnest money plus down payment) ranging from PKR 1 Million to PKR 3 Million. This is the sweet spot for most middle-class families entering the market for the first time.

If your growing family requires a bit more space, you might set your sights on a 10 Marla house. For a property of this size, your total deposit requirement will comfortably jump to between PKR 3 Million and PKR 7 Million.

Of course, these numbers fluctuate based on several massive factors. Location is the biggest variable. A 5-marla house in a highly sought-after, Premium area like Johar Town or DHA will demand a significantly higher deposit than a similar-sized house in a newly developing suburban scheme. Additionally, you must always factor in inflation, which continuously drives up the baseline prices of raw materials and, consequently, finished homes.

Factors Affecting Your House Initial Deposit

Your journey to homeownership is unique to you. The numbers we discussed above are great averages, but your specific situation will ultimately dictate your required deposit. Let’s personalize this and look at the real-world factors that will affect your wallet.

Income, Credit, and Loan Schemes

Your personal financial profile is the first thing banks look at when determining your required down payment.

- First-Time Buyers: If you have never owned a home before, you are in a great position. Through government initiatives Housing program, first-time buyers can secure mortgages with down payments as shockingly low as 5% to 10%, thanks to heavy state subsidies.

- Bank Requirements: If you are taking a traditional route through major commercial lenders like MCB or Arif Habib, the rules are stricter. These traditional banks generally require a minimum 20% down payment to minimize their lending risk.

- Credit Score Impact: Yes, your credit history matters immensely now! A strong Consumer Information Bureau (CIBIL) score or credit history proves to the bank that you are a trustworthy borrower. Excellent credit can often help you negotiate your required deposit down to 15%.

Market Trends

You cannot ignore the broader economy when buying a house. In 2026, the real estate market is heavily influenced by rising interest rates. When the central bank raises interest rates, traditional mortgages become much more expensive to pay off monthly. To compensate for this, many banks are raising their initial deposit requirements, forcing buyers to put more money down up front to reduce their monthly burden.

However, it is not all bad news. To combat these rising rates, government-backed housing schemes have strategically stepped in to cap initial deposits at 20% for eligible lower- and middle-income families, keeping the dream of homeownership alive amid economic turbulence.

Step-by-Step: Calculating Your Initial Deposit

Does all this math have your head spinning? Do not worry. Calculating your required funds is actually a very straightforward process once you break it down. Grab a piece of paper, a pen, and your smartphone calculator. Let’s walk through an actionable guide to finding your magic number.

- Step 1: Determine the Base Down Payment. First, find the property’s total asking price. For a safe, traditional bank loan, multiply the total price by 20% (0.20). This gives you the base down payment you require.

- Step 2: Calculate the Earnest Money. Next, take that same total property price and multiply it by 1% (or 0.01). This is the earnest money you need to hand over the moment your offer is accepted.

- Step 3: Combine for Your Total. Add the results of Step 1 and Step 2 together. This final number is the absolute total amount of liquid cash you need to have ready before you sign any contracts.

Let’s look at a real-world example: Imagine you find a beautiful home listed for PKR 15 Million (1.5 Crore).

- Down Payment: PKR 15,000,000 × 20% = PKR 3,000,000

- Earnest Money: PKR 15,000,000 × 1% = PKR 150,000

- Total Initial Deposit Needed: PKR 3,000,000 + PKR 150,000 = PKR 3,150,000

To make this even easier, we recommend using a free online PKR deposit calculator. These handy digital tools let you enter the property price and instantly see your required cash breakdown, saving you time and stress!

Government Schemes Lowering Initial Deposits

Saving up millions of rupees is a daunting task for anyone. Fortunately, as we navigate through 2026, you do not necessarily have to do it all on your own. You can leverage trending government programs designed specifically to ease your financial burden.

If you qualify for these programs, your required initial deposit can drop to as low as 5%. That means on a PKR 10 Million home, you would only need PKR 500,000 to get started, rather than the standard 2 Million!

Who gets these amazing benefits? The eligibility criteria are quite strict but very fair. Generally, these programs target individuals with a verified monthly salary of less than PKR 100,000. Furthermore, there is often a geographical priority system in place; for instance, verified, long-term residents are currently being prioritized for upcoming housing developments on the outskirts of the city.

First-Time Buyer Incentives

Even if you do not qualify for the low-income subsidies, the government still wants to encourage you to buy. In 2026, there are fantastic first-time buyer incentives wrapped into the tax code.

If you are purchasing your first home, you can apply for significant tax rebates on initial deposits of PKR 1 Million or More. When you file your annual taxes, the Federal Board of Revenue (FBR) will credit a portion of your deposit back to you, effectively lowering the overall cost of your home acquisition. Always speak to a certified tax consultant to ensure you claim every rebate you deserve!

Tips to Save for Your House Down Payment

Knowing how much you need is only half the battle; actually saving the money is where the real work begins. If you are starting from zero, do not panic. Here are some highly practical, actionable hacks to build your down payment for your house faster than you thought possible.

- Automate Your Savings: The best way to save is to remove the temptation to spend. Set up monthly Systematic Investment Plans (SIPs) in a high-yield savings account, such as an HBL savings account. Have a set amount automatically transferred from your checking to your savings the very day you get paid.

- Pool Family Resources: culture, family is everything. Do not be afraid to look into family pooling. Many young couples successfully buy their first home by combining their savings with those of their parents or siblings. Just ensure everything is documented clearly to avoid future disputes!

- Liquidate Unnecessary Assets: Do you have an older second car sitting in the driveway? Do you own plots of raw land in remote areas that you are not using? Sell those assets and funnel that cash directly into your house fund.

- Avoid Overpaying Agents: Be fiercely protective of your cash. Negotiate your real estate agent’s commission upfront. A common pitfall is paying a standard 2% fee when the agent might be perfectly willing to accept 1% if asked firmly. That 1% savings translates to hundreds of thousands of rupees staying in your pocket!

Common Mistakes with Initial Deposits

When large sums of money are changing hands, the margin for error is incredibly thin. Mistakes during the deposit phase can cost you your dream home and your life savings. We want to warn you about the most common traps so you can avoid them entirely.

Skipping the Lawyer Review

This is the absolute biggest mistake buyers make. Never hand over a massive check based on a verbal promise or a poorly written, standard-template contract. Always hire a qualified real estate lawyer to review the terms of your earnest money agreement. If the seller hides a structural defect and you want to back out, a good lawyer ensures your contract has an “escape clause” so you get your deposit back. Without legal review, you risk non-refundable losses.

Confusing Token Money with Earnest Deposit

it is common to give a small cash sum—say, PKR 50,000—to get the seller to stop showing the house for a few days. This is known as “token money.”

Do not confuse token money with your actual, legally binding earnest deposit (Bayana). Token money is often informal and highly susceptible to scams. Ensure that, once you move past the token stage, your full earnest deposit is properly recorded on stamped legal paper with witnesses present.

FAQs

To wrap things up, let’s address some of the most frequently asked questions about initial property deposits floating around the internet.

What is the initial deposit when buying a house? the initial deposit is the upfront cash required to buy a property. It typically consists of a 1% to 2% earnest money payment (Bayana) paid at the agreement stage, followed by a 20% down payment required by banks before transferring possession. For a PKR 1 Crore house in expect to need around PKR 2 Million to PKR 2.5 Million in total.

Is earnest money part of the down payment? Yes, in most standard real estate transactions, your earnest money counts toward your final down payment. Think of the earnest money as an early, partial installment. When you sit down at the closing table, the earnest money you already paid will be subtracted from the total down payment amount you owe.

What is the minimum deposit for a 1 Crore housing scheme? If you qualify for low-income government initiatives like the Mera Ghar scheme, the minimum deposit for a PKR 1 Crore (10 Million) house can be as staggeringly low as 5%. This means you would only need to provide PKR 500,000 upfront, making homeownership incredibly accessible for middle-class families.

How do I recover my deposit if the deal cancels? You can only recover your deposit if your initial purchasing contract includes specific contingencies (escape clauses). For example, if your contract states that the purchase is contingent on a clear property inspection and the inspector finds extensive termite damage, you are legally entitled to a full refund of your earnest money. Always have a lawyer draft these protective clauses!

What are the deposit trends ? In 2026, we are seeing a dual trend. Traditional commercial banks are slightly raising their deposit requirements (often demanding 20% to 25%) to combat high national interest rates. Conversely, government-subsidized programs are simultaneously lowering deposit barriers (down to 5% to 10%) to encourage first-time buyers to stimulate the economy. Your experience will depend entirely on which financing route you choose!