If you currently live in a council house and are considering buying a home, you may wonder if it’s possible to keep your council tenancy while owning another property. Generally, council housing rules require tenants to use the council property as their only or main home, and owning another house can affect your eligibility to remain in the council property. The Right to Buy scheme allows secure council tenants to purchase their council home at a discount, but once you own a property, continuing to live in a council house simultaneously is usually restricted by tenancy agreements. However, specific rules and exceptions can vary depending on your local council and whether you qualify for schemes like Right to Buy or Preserved Right to Buy. It’s important to understand these rules fully before making any decisions about buying a house while living in council accommodation.

Understanding the concept of council housing

Council housing refers to rental properties provided by local authorities, designed to offer affordable accommodation for those in need. These homes are often subsidized, making them accessible for individuals and families with lower incomes.

Originally established post-World War II, council housing aimed to address the housing crisis and ensure everyone had a safe place to live. Today, it remains a crucial part of social welfare in many communities.

Typically, tenants enjoy security in their tenancies with rights that protect them from sudden eviction. However, there are specific regulations governing these properties—like restrictions on subletting or selling.

Living in a council house can provide stability but may also come with limitations when pursuing homeownership options. Understanding these nuances can help clarify your path if you’re considering buying while still residing in one of these homes.

Can you buy a house while still living in a council house?

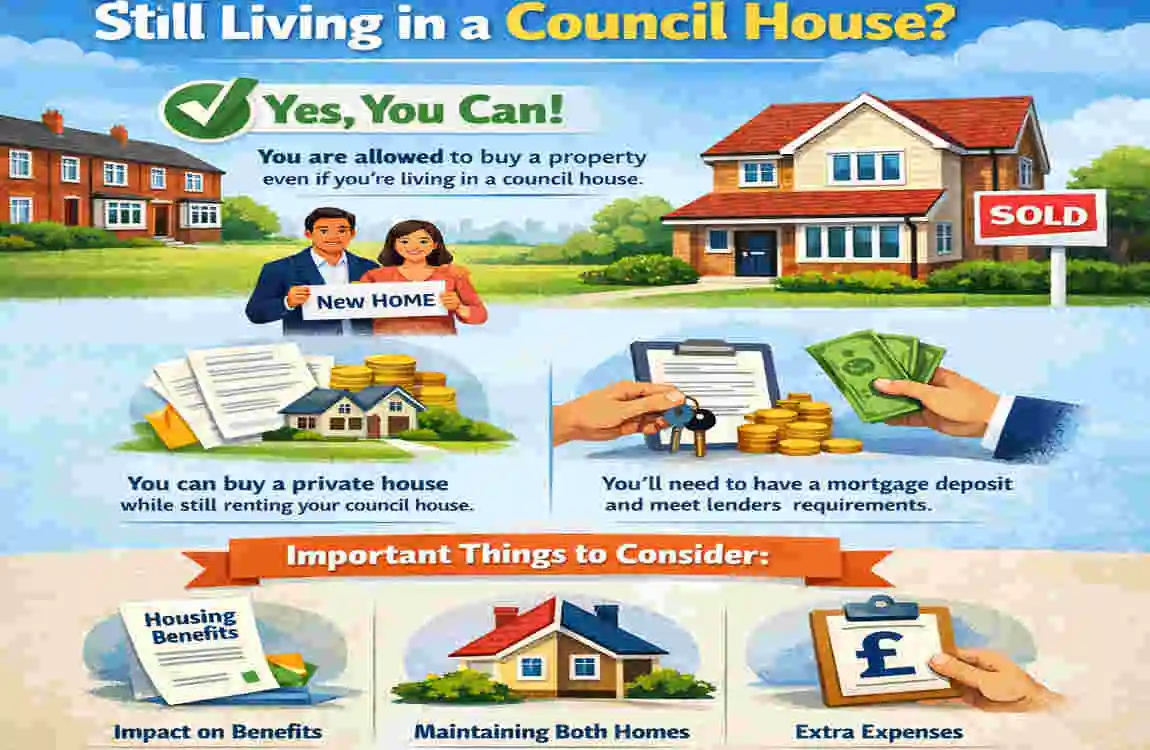

Buying a house while living in a council house is possible, but it comes with important considerations. Many tenants wonder if they can have both properties simultaneously.

If you decide to purchase a home, you typically need to relinquish your council tenancy. Council rules often prevent individuals from owning private property and keeping their subsidized housing.

However, there are situations where you might be able to transition smoothly into homeownership through schemes like Right to Buy. This allows long-term council tenants the chance to buy their homes at discounted rates.

It’s essential to check local regulations and speak with your housing officer for specific guidance tailored to your circumstances. Balancing ownership dreams with current living arrangements requires careful planning and understanding of all options available.

The right to buy scheme and its eligibility criteria

The Right to Buy scheme offers council tenants the chance to purchase their homes at a discounted price. This initiative aims to promote homeownership among those living in social housing.

To qualify, you must have been a tenant for at least three years. This period can include time spent in different council properties. However, certain exceptions exist; if you’ve previously owned a property or have had tenancy issues, your eligibility may be affected.

Discounts vary based on how long you’ve lived there and the property’s market value. For instance, longer tenancies typically lead to higher discounts.

Lenders often look for stability and affordability when assessing mortgage applications related to the Right to Buy scheme.

Pros and cons of buying a house while living in a council house

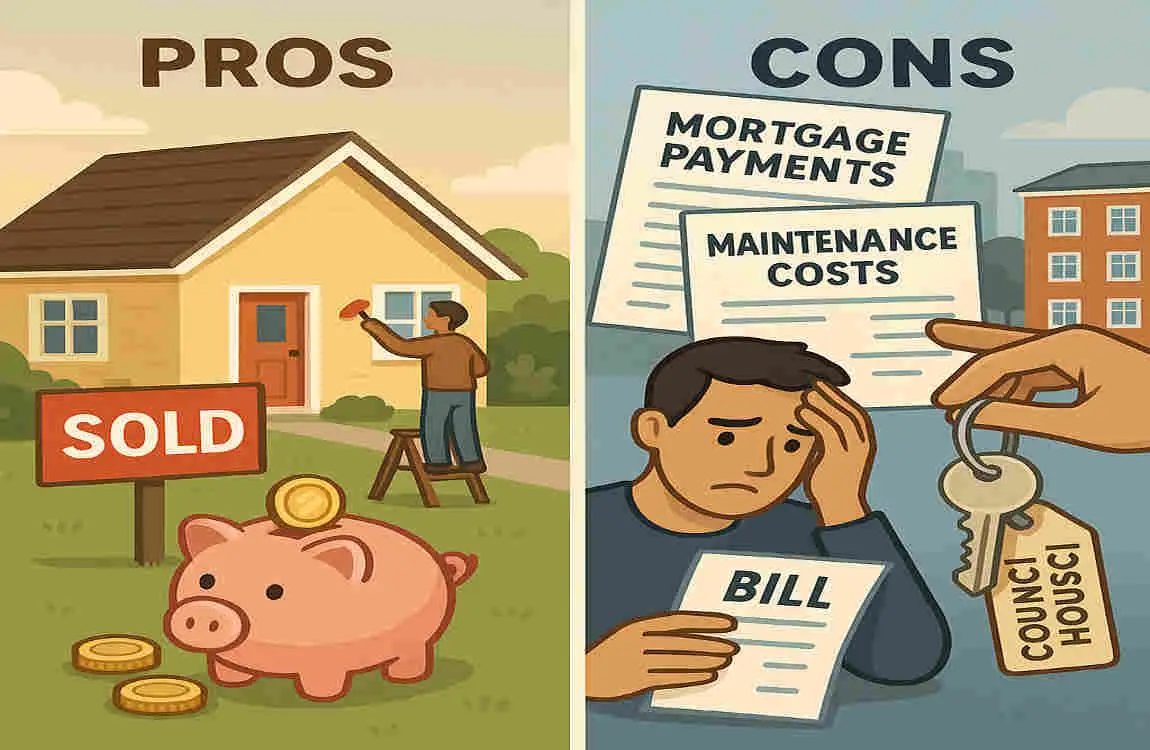

Buying a house while living in a council house has its advantages. One major benefit is the potential for homeownership stability. Owning your own property can provide you with greater control over your living situation.

Over time, homes often appreciate in value, giving you an asset that could lead to future wealth.

However, there are drawbacks to consider as well. Financial strain might arise from managing mortgage payments alongside existing rent obligations. It’s essential to assess whether you can afford both commitments without jeopardizing your financial health.

There’s also the emotional toll of making such significant changes while still tied to council housing rules and regulations. You may find yourself feeling overwhelmed by the complexities of juggling two different living situations simultaneously.

Steps to follow for purchasing a house as a council tenant

If you’re considering purchasing a house while living in a council house, start by assessing your financial situation. This includes reviewing your savings, income, and any outstanding debts. It is crucial to know how much you can afford.

Next, research the properties available for sale in the area where you wish to buy. Look at local market trends to gauge prices and potential neighborhoods that suit your lifestyle.

Once you’ve identified suitable properties, arrange viewings to get a feel for each one.Before making an offer, make sure you inspect every detail.

Contact mortgage lenders early on to discuss options tailored for council tenants. Getting pre-approved can streamline the process significantly.

Consult an estate agent or solicitor who has experience with these types of transactions. They can guide you through negotiations and paperwork effectively.

Alternatives to buying a house while living in a council house

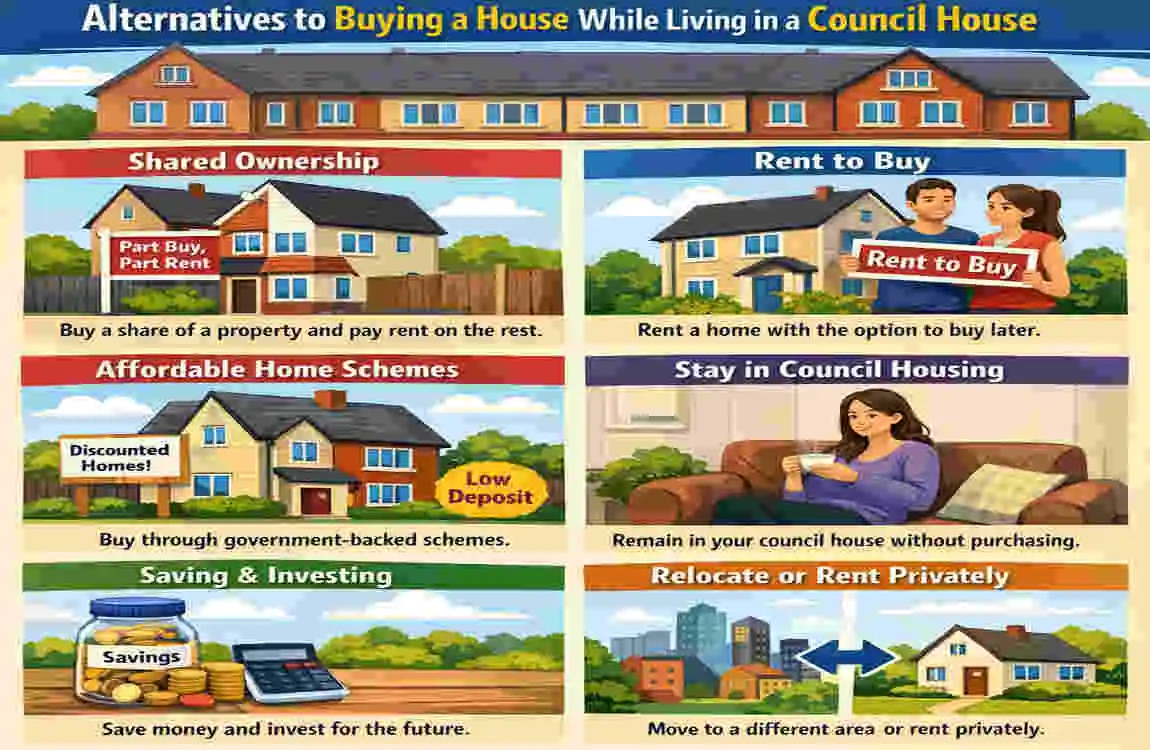

If buying a house while living in a council house doesn’t seem feasible or appealing, there are other options to consider. A more flexible alternative is to rent privately. This can offer the chance to experience different neighborhoods or housing styles without the long-term commitment of homeownership.

These allow you to buy a share of a property and pay rent on the remaining portion. It’s an affordable way to start building equity while still having access to rental support.

You may also explore housing associations, which often provide affordable rental properties with various amenities and community services. They might be less rigid than council houses in some areas but could still be within budget.

Staying informed about government initiatives aimed at assisting low-income households can open new doors. Grants, subsidies, and programs designed for first-time buyers could make homeownership more attainable down the line.

Each alternative has its own advantages and challenges, so it’s essential to evaluate what fits best with your financial situation and lifestyle preferences before making any decisions.

FAQ: Can I Buy a House and Keep My Council House?

Can I own another property while living in my council house?

In many cases, you can technically own another property, as some councils mainly require that the council house is your primary residence . However, this can raise questions about eligibility and fairness.

Will owning another home affect my council tenancy?

Yes. Owning another property can affect your entitlement to housing and other benefits, and some councils state you cannot be a council tenant and own another home .

Can I still use Right to Buy if I own another property?

No. A secure tenant cannot exercise Right to Buy unless the council home is their only residence .

Is it allowed if the second property is buy‑to‑let?

Owning a buy‑to‑let property can still affect your benefit entitlement and may be reviewed by your council .

Can I stay in my council house forever even if circumstances improve?

Many tenants keep their home for life unless they voluntarily give it up or break tenancy terms.