Hey there, if you’re dreaming of owning a home in the UK, you’re not alone. However, let’s face it, the housing market in 2025 is a challenging prospect. With average house prices soaring past £300,000 in many areas, and that’s before you factor in stamp duty and other fees, more people are asking: is it cheaper to buy land and build a house in the UK? It’s a question that’s buzzing around forums and coffee chats, especially as remote work makes rural spots more appealing.

Picture this: instead of settling for a cookie-cutter house that doesn’t quite fit your needs, you buy a plot of land and create something custom-made. This idea is gaining traction because building home allows you to control costs, design, and even energy efficiency. In 2025, with inflation easing but material costs still high, self-building is seen as a smart alternative for savvy buyers.

But hold on, is it really cheaper? That’s the big question we’ll tackle head-on. We’ll dive into a comprehensive cost comparison between buying land and building versus acquiring an existing property. We’ll break down the numbers, weigh the pros and cons, and share insider tips to help you decide.

In 2025, the UK government is pushing self-build initiatives with schemes like the Right to Build registers, making it easier to find plots. Yet, challenges like planning permissions and rising labor costs persist. Our goal here is to arm you with facts, so you can make an informed choice without the guesswork.

Understanding the Costs: Buying Land vs. Buying an Existing Home

What Buying Land Entails in the UK

Buying land in the UK isn’t just about selecting a spot and paying the price. You start by finding a plot, which could be anything from a rural field to an urban brownfield site. The process involves searches, surveys, and often securing planning permission, which is the official approval required to build.

Costs kick off with the land price itself. In 2025, expect to pay anywhere from £50,000 for a small rural plot to over £500,000 in high-demand areas like London. Don’t forget stamp duty land tax, which applies if the land costs more than £150,000.

You’ll also need a solicitor for legal checks, adding £1,000 to £2,000. And if the land doesn’t have planning permission, you might spend £5,000 or more on applications and appeals.

Overview of Costs for Purchasing an Existing House

Switching gears, buying an existing home is more straightforward but often pricier upfront. In 2025, the average UK house price hovers around £285,000, up slightly from last year due to steady demand.

Add in stamp duty – for a £285,000 home, that’s about £4,250 for first-time buyers. Then there’s conveyancing fees (£1,500-£2,500), surveys (£400-£1,500), and moving costs (£1,000+).

You’re buying a finished product, so no house construction worries, but you might face renovation bills if the place needs work.

Breakdown of Typical Land Prices by Region and Type

Location is everything when it comes to land prices. In rural Scotland or Wales, you might secure a plot for £20,000 to £100,000, perfect for a cozy self-build.

Urban areas tell a different story. In southeast England, expect £200,000-£1 million for city-adjacent land. Brownfield sites (previously developed) can be cheaper but come with cleanup costs.

Planning permission status boosts value – land with outline permission can cost 20-50% more. For example, a permitted plot in the Midlands might run £150,000, versus £100,000 without.

Factors Affecting Land Prices

Several things drive up land costs. Proximity to amenities like schools and transport jacks up prices – think £300,000+ near London commuter belts.

Soil quality and flood risk are also important considerations. Poor ground could add £10,000 to the cost of foundation work. In 2025, eco-regulations favor sustainable sites, potentially lowering costs with grants.

Market trends play a role; post-Brexit supply chains have stabilized, but demand for self-build plots is rising, resulting in yearly price increases of 5-10%.

Summary Comparison: Upfront Costs

So, let’s compare apples to apples. Buying land can cost between £100,000 and £300,000 upfront, plus an additional £10,000 in fees. An existing home? £285,000 average, with £10,000-£15,000 extras.

Land seems cheaper initially, but remember, you still need to build. For a family home, total costs could equal or exceed the cost of buying a ready-made home. Yet, if you score a bargain plot, savings await.

Construction Costs: Building Your Own Home in the UK

Overview of Construction Cost Components

Once you’ve got the land, the real fun begins: building. Construction costs break down into materials, labor, and permits. Materials such as bricks, timber, and insulation form the bulk – accounting for approximately 40-50% of your budget.

Labor comes next, with builders, electricians, and plumbers charging by the hour or project. Permits include building regulations approval, which ensures your home is safe and up to code.

In 2025, expect to budget for eco-friendly extras, such as solar panels, driven by net-zero goals.

Average Cost per Square Foot/Metre for Building in 2025

Let’s talk numbers. The average build cost in the UK is £1,500-£3,000 per square metre, depending on specs. For a 100 sqm home, that’s £150,000-£300,000.

In rural areas, it’s cheaper – around £1,200/sqm – while urban builds hit £2,500/sqm due to access issues. These figures include VAT at 20%, a big chunk.

Compared to 2024, costs are up 3-5% due to inflation, but efficiencies in modular building are helping offset this increase.

Impact of Home Size, Design Complexity, and Material Choices

Size matters a lot. A compact three-bedroom house costs less than a sprawling five-bed. Every extra metre adds £1,500 to £3,000.

Design complexity ups the ante. Fancy curves or custom features? Add 10-20% to your bill. Stick to simple shapes for savings.

Materials make a difference, too. Opt for budget bricks over premium stone, and you’ll shave off thousands. Sustainable choices, such as those made with recycled materials, may qualify for rebates, thereby helping to balance costs.

Hidden Construction Costs to Expect

Don’t overlook the sneaky extras. Planning fees start at £462 for a full application, plus architect’s drawings (typically £5,000-£10,000).

Council charges for inspections add up, and builder fees include profit margins of 10-15%. Site insurance is essential – £1,000 to £2,000 per year.

Unexpected groundworks, like drainage, can cost £10,000 if issues arise.

Timeline Impact on Costs and Inflation Risks

Building takes time – typically 6 to 12 months. Delays from weather or supply chains can inflate costs; a month’s holdup might add £5,000 in labor costs.

In 2025, inflation is projected to be 2%, making it beneficial to lock in prices early. Staged builds allow you to manage cash flow, but they also risk price hikes.

Case Study Examples with Cost Breakdowns

Let’s look at real examples. Take Sarah from Yorkshire: She bought a £80,000 rural plot and built a 120 sqm eco-home for £220,000 total. Breakdown: Materials £90,000, labor £80,000, permits £10,000, extras £40,000.

In contrast, Tom in London spent £450,000 on a 150 sqm urban build: Land £300,000, construction £150,000. His complex design added £20,000.

These show how location and choices swing costs. Imagine your own project – what size home do you envision?

Here’s a quick table to visualize a sample cost breakdown for a standard 100 sqm home:

Cost Component Estimated Cost (2025)Notes

Materials £60,000 – £100,000 Includes basics like bricks and roofing

Labor £50,000 – £80,000 Builders, electricians, etc.

Permits & Fees £5,000 – £10,000 Planning and regulations

Architect/Design £5,000 – £15,000 Custom plans

Total £120,000 – £205,000 Excludes land

Additional Costs Beyond Land and Construction

Building a house doesn’t stop at walls and a roof. There are plenty of add-ons that can sneak up on you. Let’s break them down so you’re prepared.

First up, surveys and feasibility studies. Before you dig, a land survey checks for issues such as soil stability and boundaries. In 2025, these costs will range from £500 to £2,000. A feasibility study, which assesses whether your plans are viable, adds an additional £1,000-£3,000.

Legal fees are non-negotiable. For land purchase, solicitors typically charge between £1,000 and £2,500. Construction contracts also need reviewing, with an additional £500-£1,500 to ensure everything’s airtight.

Utility connections are a big one. Hooking up electricity, water, and sewage isn’t free. Expect £2,000-£10,000, depending on distance from mains. Rural areas might require septic systems, which can increase costs to £ 5,000 or more.

Don’t forget the outside stuff: landscaping, driveways, fences, and external works. A basic garden setup runs £5,000-£15,000. Driveways? £3,000-£8,000 for gravel or paving. Fences add £1,000-£3,000 for privacy.

Insurance and contingencies wrap it up. Build insurance covers accidents (£1,000-£2,000 annually). Set aside 10-15% of your budget for surprises – that’s £20,000 to £50,000 on a £200,000 build.

Financial Considerations and Funding Options

Financing a self-build project differs from financing a standard home purchase. Let’s explore how to fund it without overspending.

Mortgages for land are trickier. Lenders offer them, but with higher interest, around 4-6% in 2025. You may need a 25-40% deposit, unlike the 5-10% required for homes.

Home mortgages are more straightforward, with rates typically ranging from 3% to 5%. But for building, you want construction loans. These release funds in stages – first land, then build phases – keeping interest rates lower.

Staged payment plans help cash flow. Pay as you go, but be aware of potential delays that can increase borrowing costs.

Good news: grants and subsidies exist. The Self-Build and Custom Housebuilding Act provides access to plots, and eco-grants, such as the Green Homes Grant, can offer a rebate of up to £5,000 for sustainable features.

Tax reliefs include VAT reclaim on materials for new builds – up to 20% back. That’s huge savings!

Resale value is key. A custom home might sell for 10-20% more than its cost, especially if it is energy-efficient. But factor in market dips; 2025 forecasts stable growth.

Consider your finances, reader. Could a construction loan fit your budget?

Here’s a list of funding options:

- Self-build mortgages: Staged funding from lenders like Ecology Building Society.

- Government schemes: Right to Build for plot finding.

- Bridging loans: Short-term for land buys.

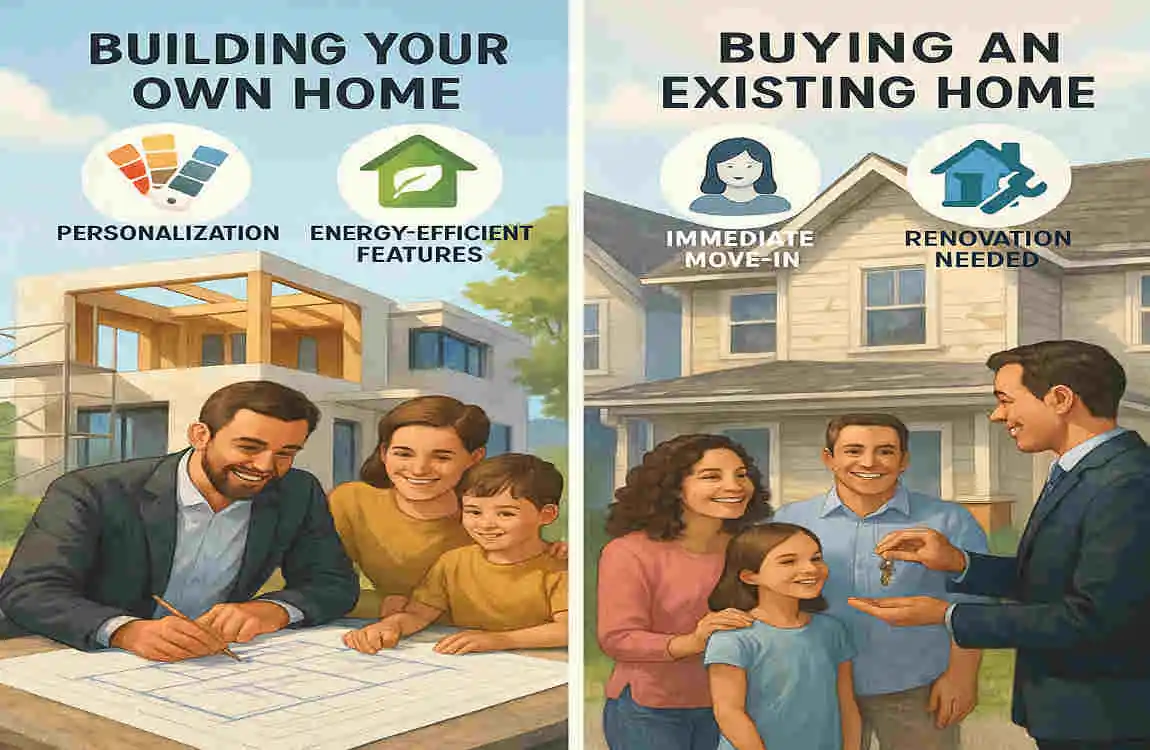

Advantages of Building Your Own Home vs Buying an Existing Home

Building your own home lets you customize every detail. Do you want an open-plan kitchen or a home office? You decide, making it future-proof for your family’s needs.

Energy efficiency is a win. In 2025, new builds must meet high standards, incorporating insulation and renewable energy sources. This slashes bills – up to 30% less than older homes.

Long-term maintenance savings add up. Fresh materials mean fewer repairs; no dealing with someone else’s leaky roof.

Emotionally, it’s rewarding. Imagine the pride of creating your space. Lifestyle perks include better layouts for hobbies or accessibility.

Disadvantages and Risks to Consider

Self-building takes time – months of planning and oversight. It’s complex, juggling contractors and decisions.

Budget overruns are common, with 20-30% of extras resulting from unexpected surprises. Delays due to weather or permits can stretch timelines.

You need expertise. Without project management skills, mistakes happen. Hiring a manager adds costs.

Market volatility risks resale; if prices drop, your investment suffers.

Insider Tips to Save Money When Building in the UK

Negotiate land prices by researching comparables and making an offer below the asking price. Choose plots with existing permissions to skip fees.

Select reliable builders via reviews and quotes from three sources. Check certifications for quality.

Optimize design: Go modular for speed and savings – up to 20% cheaper.

Plan thoroughly with realistic budgets that include buffers. Use apps for tracking.

Leverage schemes like local council advice for free guidance.

Is It Cheaper? Final Cost Comparison and Verdict

Summing up: For a £200,000 existing home, the total cost, including fees, is £220,000. Land (£100,000) plus build (£150,000) plus extras (£30,000) totals £280,000 – pricier initially.

However, in rural areas, land at £50,000 and an efficient build at £120,000 could result in a total of £ 170,000, which is cheaper.

Building saves when customizing or in low-cost regions; buying is better for quick moves.

Consider your goals – if long-term savings are a priority, build. Expert advice: Research, consult professionals, and make a decision for 2025.